Guides & best practices

View all articlesHow to build a mortgage lead funnel for paid marketers

If you’re running paid ads for mortgage leads, you’ve probably seen this pattern: a steady stream of clicks, plenty of form fills, and almost no qualified borrowers. You check the data and realize that the qualified leads you paid for are bots, bored browsers, or people who just wanted to check their eligibility.

Paid mortgage campaigns are hard to get right because the post-click experience breaks long before the sales team ever touches a lead.

To understand what’s really going on, we spoke to Amir Bohnenkamp, Co-founder & CEO at Heyflow, and Andrea Monti Solza, Co-founder at Conveyo, about what today’s buyers actually feel, how they behave online, and why so many funnels collapse between the ad click and the borrow-ready moment. Their insights shape this guide end to end.

What follows is a practical breakdown of how to build a high-performing mortgage lead funnel by:

Pre-qualifying leads early, without adding friction

Cutting wasted ad spend and filtering out low-intent traffic

Building a post-click flow that actually moves people forward

Shaping your funnel around what today’s buyers are really dealing with

So before you pour another dollar into ads, let’s see where your funnel might be failing you.

Why mortgage lead generation is challenging for paid marketers

The mortgage industry runs on trust, timing, and compliance — three things that don’t always align with the pace of digital marketing.

And behind the numbers, there’s a bigger emotional shift you’re advertising into.

For previous generations, buying a home was an ordinary life step, predictable, affordable, and not an identity-defining milestone. Today’s buyers, especially Millennials and Gen Z, experience homeownership as a psychological saga… a long, emotionally charged journey filled with doubt, compromise, and the constant question: ‘Will this ever be possible for me?’ You’re not just fighting CPCs. You’re fighting a deep sense that ‘the system isn’t built for you.

– Andrea Monti Solza, Co-founder at Conveyo

Here’s why that makes mortgage lead generation so hard to scale.

1. Clicks are expensive, and lead quality rarely keeps up

Finance and real estate carry some of the highest Google Ads costs. According to Digital Position’s 2024 PPC benchmarks, the U.S. average cost per click (CPC) sits around $4.18, with mortgage-intent keywords among the costliest.

When every click costs that much, each lead form submission must deliver real value. Yet many campaigns still produce unverified or low-intent contacts, leaving mortgage lenders paying premium prices for poor data.

Andrea’s observation at the journey level explains part of this mismatch. He says:

You’re paying performance-level prices to speak to people who are still stuck in ‘Will this ever be possible for me?’ rather than ‘Who should I apply with?’

2. Mortgage marketing is built on authority and social proof

Borrowers look for visible Nationwide Multistate Licensing System (NMLS) identification numbers, authentic reviews from past clients, and consistent branding before they ever click “Submit.”

Without visible licensing details, verifiable testimonials, or genuine social proof, even high-converting interactive landing pages can lose qualified leads instantly.

But in a category that feels opaque and untrustworthy to most buyers, Andrea argues that traditional trust signals only land after an emotional connection:

Competence isn’t a differentiator: everyone claims competence. Emotion is the differentiator.

The first job of your TOFU experience isn’t to recite credentials. It’s to provoke a rare reaction in this space: ‘Whoa. I like this. Tell me more.’ Authority and social proof work best once that instinctive ‘this feels like it’s for me’ moment is in place.

4. Forms ask for too much, too soon.

Most mortgage landing pages ask for credit score, income, or property value right away, creating friction that pushes away potential qualified leads. But if you simplify too much, you waste time on unfit purchased leads. The challenge in modern lead generation is balancing qualification and experience: capturing high-intent leads without scaring them off.

Andrea is clear on what doesn’t work with younger buyers: Any tone that treats Millennial/Gen-Z buyers like they’re naïve.

Millennial/Gen-Z buyers already know the system is stacked against them. They know the journey is long, uncertain, and emotionally draining. So when brands paint a rosy picture — “it’s easy!”, “just save!”, “your dream home is within reach!” — it feels insulting. It shows you don’t understand their lived reality.

Equally, doomscrolling negativity fails too. They don’t need another reminder of how bad things are. Relentless pessimism just creates distance.

What makes them lean in is optimistic realism. A tone that says:

“Yes, this is hard, and here’s what we can do to make it a bit easier."

“You’re not imagining the challenges. But here’s how to navigate them successfully.”

“Here’s how the process can be made clearer, fairer, and more manageable.”

This generation responds to brands that respect their intelligence, acknowledge the structural truth, and offer a path forward that feels grounded, not delusional.

“We see what you see, and we’re here to help you navigate it anyway.”

5. Compliance rules restrict creativity

Mortgage ads are governed by the Truth in Lending Act (TILA), Regulation N (MAP Rule), and the Fair Housing Act. Every claim must be backed by clear disclosures, and every creative must display lender licensing.

You can’t make unverified rate claims or exclude protected groups in targeting. For mortgage brokers and loan officers, that means longer review cycles, stricter ad copy, and limited testing flexibility, all of which slow down lead generation efforts.

In simple words, you need a system that turns the traffic you already have into qualified borrowers. To fix that, you need to understand what an effective mortgage lead funnel looks like from start to finish.

What does the mortgage lead funnel look like?

To understand how the mortgage funnel behaves, it helps to see how fast other industries are evolving and why mortgage still resists that pace.

Across B2C categories, generative AI is reshaping how shoppers research, compare, and decide. Adobe reported a 4,700% year-over-year increase in AI-driven visits to eCommerce sites by July 2025, and those AI-assisted visitors showed stronger engagement: +32% longer sessions and −27% lower bounce rates. These numbers prove that consumer funnels are getting smarter and faster.

The mortgage marketing journey, by contrast, remains multi-stage and documentation-heavy.

A typical progression of marketing lead capture looks like this:

Pre-qualification → application → processing → underwriting → approval → closing

With steep drop-offs between pre-qualification and application, and again between application and approval, as credit checks, income proofs, and rate fluctuations often derail even high-intent leads.

Andrea’s version of this journey is even more honest. If you draw it the way buyers experience it, not the way the industry decks describe it, you get:

The early emotional phase: A messy, multi-year mix of identity formation, income insecurity, aspirational dreaming, and fear of missing out or messing up. This is where anxiety starts, long before any “lead” appears.

The long preparation phase: Five to ten years of saving, compromising, despairing, recalibrating. Dipping in and out of portals, browsing endlessly with no action, flirting with possibility, then pulling back. This oscillation is the real funnel.

The chaotic decision phase: The industry pretends this is “search → viewing → offer → legal → completion”. Buyers experience “hope → panic → confusion → rushing → regret → paperwork → silence → more panic”.

The ownership phase: Maintenance, insurance, remortgaging, renovations, neighbour issues, life transitions, all handled through a patchwork of siloed providers.

The repeat cycle and legacy: Job changes, children, divorce, relocation, upsize, downsize, inheritance, care, death. The loop repeats with more emotional and financial baggage each time.

What are the types of mortgage leads you’re looking to attract?

Not all potential leads behave the same, and knowing who’s entering your lead magnet funnel determines how you design your sales funnel, message your ads, and qualify submissions through each lead form.

Below are the primary borrower categories most mortgage businesses target today and what paid marketers need to know about each.

Lead type | Who they are | Behavior and motivation | Strategies for mortgage lead generation |

|---|---|---|---|

First-time buyers | Entering the mortgage process for the first time Often, younger or newly married buyers in local markets | Research-heavy Use search engines, social media posts, and affordability tools Need education and trust before applying | Simplify lead forms Highlight educational content Use marketing automation for nurturing and consistent follow-up |

Move-up / trade-up buyers | Current homeowners looking to upgrade | Compare lenders, monitor market trends, and visit real estate listings before submitting | Use social media marketing and retargeting Emphasize equity leverage and rate-lock programs Connect marketing systems to track leads across sell/buy stages |

Downsizers / retirees | Empty nesters or retirees looking to reduce costs or access equity | Value-driven Rely on credibility and referrals May consult financial advisors | Build trust with social proof Optimize for accessibility Use personalized follow-up and simple calls-to-action (CTAs) to convert leads |

Investors / second-home buyers | Experienced borrowers purchasing rental or vacation homes | Fast-moving Data-driven Seek exclusive leads and high returns | Route high-quality leads forward immediately Use marketing automation and calculators Display ROI, rental income, and past client success |

Refinance / equity release | Homeowners refinancing or cashing out equity | Highly rate-sensitive Want quick responses Act fast when savings are clear | Keep sales funnels short Capture leads through one-click pre-qualified forms Automate follow-ups to improve conversion rates |

Specialty segments (VA, FHA, jumbo, non-QM) | Military members, low-income borrowers, or self-employed | Seek expertise and specific qualification info Value compliant, knowledgeable lenders | Create program-specific funnels and social media marketing campaigns Display certifications Use targeted lead forms for precise lead conversion |

How to build a mortgage lead funnel with paid ads in 7 steps

Now that you know who your potential leads are and what each expects from the funnel, it’s time to design a system that consistently attracts, qualifies, and converts them. Let’s walk through the seven essential steps for building a high-converting funnel using paid ads for mortgage leads.

Step 1: Identify leads and where they hang out

By now, you already know who your target borrowers are. The next step is mapping where they actually live online.

Think beyond demographics. A 35-year-old first-time buyer could be watching budget home-renovation reels on Instagram or TikTok, searching “how much mortgage can I afford” on Google, scrolling Reddit threads about rate drops, or even prompting ChatGPT or Perplexity for lender comparisons, all within the same day.

The challenge is connecting those signals to buying intent.

Start by asking three questions:

Where do they research? Are your ideal borrowers hanging out on Reddit, TikTok, or YouTube? Or are they searching through rate calculators and comparison tools on Google?

What triggers their activity? Major life milestones, such as marriage, relocation, new jobs, or having kids, often coincide with early mortgage research.

Who do they trust? Is it online reviewers, influencers, brokers, or creators who break down the fine print in plain language? Knowing who shapes their decisions tells you where to place your message.

Step 2: Run paid ads to build brand awareness

Here’s how you can structure paid ads:

Choose reach-based channels. YouTube, Connected TV, and Meta’s Advantage+ placements still offer the broadest visibility. TikTok and Reddit boost recall among younger first-time buyers.

Lead with confidence, not interest rates. At this stage, creatives should focus on credibility cues like visible NMLS ID, social proof, licensed-in-states badge, and short customer testimonial lines.

Andrea warns against two extremes: sugar-coating (“it’s easy!”) and doom (“you’ll never afford this”). Aim for optimistic realism: “Yes, this is hard – here’s how we can make it less confusing.”

Use soft CTAs. “Check your buying power” or “See how much home you could afford” perform better than “Apply now.”

Track view-through influence. Measure lifts in branded search and direct traffic rather than expecting instant applications.

Example: Rocket Mortgage’s awareness engine

Rocket Mortgage’s 2021 Super Bowl campaign (Certain is better) is a textbook example of using high-impact paid media to dominate recall.

Two 60-second spots starring Tracy Morgan, with cameos from Dave Bautista, Liza Koshy, and Joey Bosa, used humor to dramatize how dangerous “pretty sure” can be when buying a home. The message landed. Rocket didn’t just purchase visibility; it owned the conversation.

What they achieved from this campaign:

Ranked #1 and #2 on USA TODAY’s Ad Meter 2021, the first brand in over a decade to sweep the chart

Drove massive social engagement through influencer tie-ins and the Super Bowl Squares giveaway, awarding $1.6 million to 14 winners

Reinforced Rocket’s value proposition around clarity and qualification confidence, a message that continued driving search and brand lift long after game day

Cemented Rocket as the benchmark for creative, emotionally intelligent mortgage marketing, proof that humor and trust can sell a financial product better than APRs ever will

Step 3: Build (and test) high-quality landing pages

Paid search delivers high-intent visitors—people actively comparing mortgage lenders—but it’s also brutally competitive. With finance among the most expensive ad categories on Google (average CPC ≈ $4.18 in the US), you’re paying premium rates for every visit. Those clicks need a seamless, credible experience that immediately signals trust and makes it effortless to take the next step.

Paid social, on the other hand, offers cheaper reach but far lower intent. And with social platforms reporting that well over 94.4% of their traffic comes from mobile, any slow page, clunky form, or non-responsive layout kills conversions fast. That’s where most campaigns bleed money.

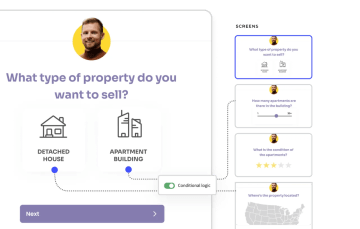

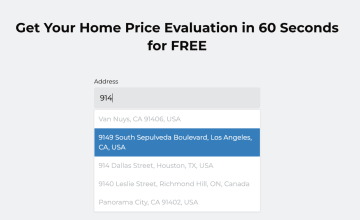

That’s why marketers in real estate and financial services are turning to Heyflow. With Heyflow, you can build interactive, mobile-first funnels that guide visitors step-by-step through questions, pre-qualify them in real time, and sync clean data directly to your customer relationship management (CRM) systems.

Real estate teams using Heyflow have reported up to 42% higher conversion rates and 31% lower cost per lead, thanks to features like conditional logic, address auto-complete, phone-number validation, and instant property-value calculators.

Its drag-and-drop builder means no dev work, lightning-fast load speeds, and total brand control, so you can launch, run A/B tests, and optimize multiple variants in minutes.

Step 4: Create a lead magnet to attract leads with specific pain points

Once you’ve built your landing page, you need a compelling reason for visitors to share their details.

Andrea is clear that younger buyers aren’t looking for “Mortgage 101” courses. They don’t want a curriculum; they want personalised clarity:

They want to be told exactly what to do based on their specific circumstances, and they want it now.

His preferred TOFU experience is interactive self-assessment wrapped in relatable storytelling. In other words:

Let them privately explore “Where do I really stand?”

Show them they’re not alone – others in their situation feel and struggle the same way

Give them one next step that doesn’t overwhelm them

Here are some examples that match that blueprint:

Affordability self-assessment tools that show realistic ranges based on their income, savings, and location

Timeline checkups that answer “How far am I from buying?” with a concrete estimate and suggested milestones

Priority-setting exercises that help them define 3–5 non-negotiables in a property (Andrea compares this to dating: everything else is noise, but those few criteria become your compass when compromises hit)

Market outlooks and neighbourhood snapshots that pair data with human narratives “Here’s what buyers like you actually did in this area”

💡Searching for inspiration? Our guide to lead magnet ideas breaks down formats that work best for different industries and intent levels.

Step 5: Collect lead information with engaging funnels

With Heyflow’s interactive funnel builder, you can guide users through short, visually engaging questions one step at a time. Each screen adapts dynamically based on their answers, so borrowers only see what’s relevant.

Here’s how Heyflow helps teams collect data more effectively:

Multi-step forms keep users focused and reduce friction, especially on mobile

Conditional logic personalizes every path (e.g., showing different fields for buyers vs. refinancers)

Phone number validation ensures fake contacts never make it into your CRM

Auto-complete address fields save time and reduce typing errors

Embedded videos create trust, letting you greet visitors face-to-face or thank them after submission

Instant calculations (like “See how much home you can afford”) turn passive form-fillers into active participants

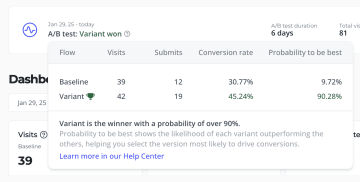

Real estate agency Book More Showings put Heyflow to the test. They rebuilt the same lead funnel across several different form builders, then ran identical Facebook ad campaigns to each version to compare performance.

Their Heyflow version used a multi-step structure with visual progress, address auto-complete, and real-time phone validation. It also loaded significantly faster between questions, especially on mobile, which was critical given that most of their paid social traffic came from smartphones. The results were striking: the Heyflow funnel converted 150% more leads, cut cost per qualified lead by 57%, and reduced setup time by half.

Step 6: Nurture leads from the get-go

How quickly you respond often determines whether that lead ever becomes a borrower. Research shared by Amir Bohnenkamp, Co-Founder & CEO at Heyflow, highlights just how steep the drop-off is:

0–3 minutes: 100% of pipeline value

3–12 minutes: 80%

30 + minutes: 70%

In other words, every minute you wait, money evaporates.

That’s why the most effective mortgage teams treat speed as a nurture strategy. A rapid, consistent first touch via phone, WhatsApp, or email can double your connect rate and set the tone for a high-trust relationship.

Set a hard internal SLA to call new leads within three minutes, and use automated fallback channels when you can’t connect right away. A simple “Thanks for reaching out, want to schedule a quick call?” message on WhatsApp or a personalized email drip can recover up to 30% of otherwise lost conversions.

This is also where Heyflow’s native integrations earn their keep. Each response collected through your funnel can automatically trigger an outreach sequence sending data straight into your CRM, launching an instant WhatsApp or email follow-up, or even firing a webhook to your dialer. Combined with phone validation and optional SMS OTP verification, you ensure you’re only chasing real leads with working numbers.

Step 7: Retarget warm leads with data-informed ads

Once a lead interacts with your funnel, clicks, fills a form, or drops off mid-way, you’ve already earned their attention. Retargeting ensures you don’t waste it.

The goal here is to feed conversion data back to your ad platforms so they can find more people who behave like your best prospects.

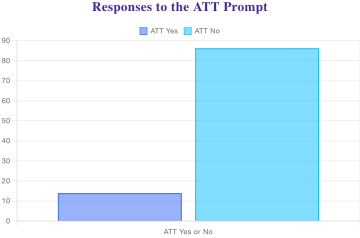

But that’s become harder since Apple’s iOS 14.5 update, which introduced App Tracking Transparency (ATT) in April 2021 and required users to opt in to cross-app tracking. Fast-forward to 2025, and the story around ATT opt-in rates has changed again, and not for the better.

According to research from Singular, opt-in rates have continued to fall: after a 16% drop in Q1 2024, rates declined another 12.5% in Q2, reaching a global “yes” rate of just 13.85%.

This number reflects immediate prompts apps that request tracking permission right at download and highlights why simply “asking early” is no longer a viable strategy.

And since users declined tracking, it immediately reduced the accuracy of browser-based pixels like Meta Pixel, TikTok Pixel, and Google Ads tags. Conversions that used to be automatically captured in-app or post-click started disappearing from dashboards, breaking audience optimization and retargeting accuracy.

Because of that, server-side tracking (also called Conversion APIs) has become the new standard. Instead of relying on a browser cookie or pixel to fire when someone converts, server-side tracking sends conversion data directly from your funnel or CRM to the ad network, bypassing blocked browsers and privacy pop-ups. It’s faster, more reliable, and fully privacy-compliant under Apple’s framework.

This is exactly where Heyflow bridges the gap. Every interaction inside your funnel—form submissions, quiz completions, or booked calls can be automatically and securely sent to all major ad platforms using native integrations. Heyflow connects directly with Meta Conversion API, TikTok Pixel, LinkedIn Insight Tag, and Voluum, ensuring your campaigns continue to learn even when browser tracking fails.

Mortgage lead funnels made easy with Heyflow

From high-cost search campaigns to mobile-first social ads, the best-performing teams win because they understand one thing: every stage of the funnel is connected. Awareness sets up consideration, consideration shapes qualification, and qualification fuels conversion.

Static landing pages, broken tracking, and delayed follow-ups create friction at every turn. Heyflow removes that friction. It helps paid marketers build interactive, mobile-optimized funnels that guide prospects step by step, validate data in real time, and feed clean, conversion-ready insights back into ad platforms.

Whether you’re generating first-time buyer leads or refinance prospects, Heyflow gives you everything you need to launch fast, test confidently, and scale what works

FAQs about mortgage lead funnels for paid marketers

What is the best way to get mortgage leads?

The best way to get mortgage leads is to combine paid ads with conversion-optimized funnels. Run targeted Google and Meta campaigns, then direct traffic to interactive landing pages or quizzes that pre-qualify borrowers and collect verified contact details.

What’s the best CRM for mortgage brokers?

Top picks include Salesforce, HubSpot, and Zoho. Heyflow makes this even easier with a no-code builder that integrates directly with these CRMs. And if you manage multiple clients or loan officers, you can even create your own white-label CRM system with a branded dashboard that lets you track, manage, and follow up on every lead without spreadsheets or external tools.

As a mortgage agent, what’s the best way to get leads?

Use local, high-intent channels like Google Search, real estate partnerships, and referral programs, supported by mobile-first lead forms. The key is fast follow-up: calling within 3 minutes can double your conversion odds.

Recommended articles

7 Typeform alternatives to help you build better B2C funnels

The most popular alternatives for Typeform specifically built for B2C marketing include Heyflow, Involve.me, Jotform, Paperform, and more.

Read more

The Best Funnel Builder for Real Estate in 2026

Transform your real estate lead generation with Heyflow's funnel builder. Double your conversion rate with interactive funnels. Free trial available.

Read more

How to Capture the Meta Click ID (fbclid) With Your Funnel

Learn how to capture the fbclid (Meta Click ID) through your funnel for precise ad attribution and offline conversion tracking. Step-by-step guide with best practices and common mistakes to avoid.

Read more